Page 184 - Profile's Unit Trusts & Collective Investments - September 2025

P. 184

Chapter 9 Fund manager interviews

Comment on the year ahead and, if possible, estimate the performance of your fund over 2 or

3 years. What are your targets and objectives for the year ahead?

We do not attempt to forecast market or fund returns over one-year periods. We continue to find a

wide disparity in valuations across different geographies and sectors, and whilst we are not overly

excited about the risk and return prospects of equity markets in aggregate, we do find it possible

to buy assets at attractive valuations that gives us confidence in the longer term returns the fund

should deliver to investors.

Are equity markets in general overpriced? Do you anticipate a significant correction?

In aggregate, we consider the world equity market to be on the expensive side of fair value. But

this is mainly due to the US market which dominates global indices. Emerging markets and some

non-US developed markets appear to offer attractive value though.

The level of the US market relative to longer term measures of value suggests that future returns

are likely to be lower than that seen over the past decade. However, we have no view as to the

likelihood of a short term correction.

Which asset classes do you expect will give the best total rates of return over the next

few years?

Global equities – but given valuations currently, we expect divergent outcomes between different

geographies within global equities.

Offshore investments are heavily influenced by the rand. Give your view on the rand over the

next 1, 3 and 5 years.

As with markets in general, we do not attempt to make short term forecasts of exchange rates. On

a longer term view, with reference to purchasing power parity, we continue to view the rand as priced

too cheaply, and hence expect rand cash investments (i.e., including interest) to be a better store of

value than many other currencies (notably the US dollar).

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

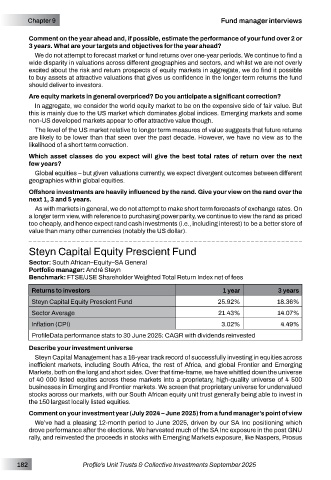

Steyn Capital Equity Prescient Fund

Sector: South African–Equity–SA General

Portfolio manager: André Steyn

Benchmark: FTSE/JSE Shareholder Weighted Total Return Index net of fees

Returns to investors 1 year 3 years

Steyn Capital Equity Prescient Fund 25.92% 18.36%

Sector Average 21.43% 14.07%

Inflation (CPI) 3.02% 4.49%

ProfileData performance stats to 30 June 2025: CAGR with dividends reinvested

Describe your investment universe

Steyn Capital Management has a 16-year track record of successfully investing in equities across

inefficient markets, including South Africa, the rest of Africa, and global Frontier and Emerging

Markets, both on the long and short sides. Over that time-frame, we have whittled down the universe

of 40 000 listed equites across these markets into a proprietary, high-quality universe of 4 500

businesses in Emerging and Frontier markets. We screen that proprietary universe for undervalued

stocks across our markets, with our South African equity unit trust generally being able to invest in

the 150 largest locally listed equities.

Comment on your investment year (July 2024 – June 2025) from a fund manager’s point of view

We’ve had a pleasing 12-month period to June 2025, driven by our SA Inc positioning which

drove performance after the elections. We harvested much of the SA Inc exposure in the post GNU

rally, and reinvested the proceeds in stocks with Emerging Markets exposure, like Naspers, Prosus

182 Profile’s Unit Trusts & Collective Investments September 2025