Page 182 - Profile's Unit Trusts & Collective Investments - September 2025

P. 182

Chapter 9 Fund manager interviews

Top three local holdings are: Pan African Resources, Telkom and Sibanye Stillwater.

On the global side, our models currently favour Robinhood, Rocket Lab and Palantir.

It is important to note that this is an active strategy: the top positions are not static but will evolve

as market and sector dynamics change. Our approach ensures we remain exposed to the strongest

performers while systematically reducing exposure to weakening trends.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

Nedgroup Investments Financials Fund

Sector: South African–Equity–Financial

Portfolio manager: Denker Capital

Benchmark: FTSE/JSE Ind/Financials index

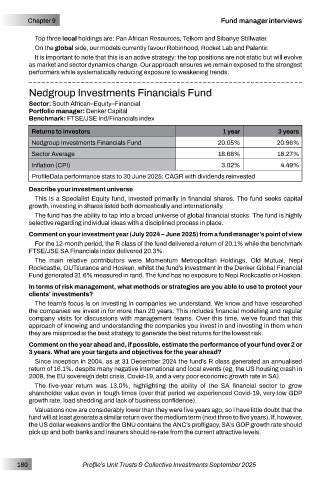

Returns to investors 1 year 3 years

Nedgroup Investments Financials Fund 20.05% 20.96%

Sector Average 18.68% 18.27%

Inflation (CPI) 3.02% 4.49%

ProfileData performance stats to 30 June 2025: CAGR with dividends reinvested

Describe your investment universe

This is a Specialist Equity fund, invested primarily in financial shares. The fund seeks capital

growth, investing in shares listed both domestically and internationally.

The fund has the ability to tap into a broad universe of global financial stocks. The fund is highly

selective regarding individual ideas with a disciplined process in place.

Comment on your investment year (July 2024 – June 2025) from a fund manager’s point of view

For the 12-month period, the R class of the fund delivered a return of 20.1% while the benchmark

FTSE/JSE SA Financials index delivered 20.3%.

The main relative contributors were Momentum Metropolitan Holdings, Old Mutual, Nepi

Rockcastle, OUTsurance and Hosken, whilst the fund’s investment in the Denker Global Financial

Fund generated 31.6% measured in rand. The fund has no exposure to Nepi Rockcastle or Hosken.

In terms of risk management, what methods or strategies are you able to use to protect your

clients’ investments?

The team’s focus is on investing in companies we understand. We know and have researched

the companies we invest in for more than 20 years. This includes financial modelling and regular

company visits for discussions with management teams. Over this time, we’ve found that this

approach of knowing and understanding the companies you invest in and investing in them when

they are mispriced is the best strategy to generate the best returns for the lowest risk.

Comment on the year ahead and, if possible, estimate the performance of your fund over 2 or

3 years. What are your targets and objectives for the year ahead?

Since inception in 2004, as at 31 December 2024 the fund’s R class generated an annualised

return of 16.1%, despite many negative international and local events (eg, the US housing crash in

2008, the EU sovereign debt crisis, Covid-19, and a very poor economic growth rate in SA).

The five-year return was 13.0%, highlighting the ability of the SA financial sector to grow

shareholder value even in tough times (over that period we experienced Covid-19, very low GDP

growth rate, load shedding and lack of business confidence).

Valuations now are considerably lower than they were five years ago, so I have little doubt that the

fund will at least generate a similar return over the medium term (next three to five years). If, however,

the US dollar weakens and/or the GNU contains the ANC’s profligacy, SA’s GDP growth rate should

pick up and both banks and insurers should re-rate from the current attractive levels.

180 Profile’s Unit Trusts & Collective Investments September 2025