Page 166 - Profile's Unit Trusts & Collective Investments - September 2025

P. 166

Chapter 9 Fund manager interviews

our credit process to assess credit risk before we assume the exposure. The fund, being a money

market fund and low risk by nature, high-quality issuers or instruments are preferred for inclusion in

the portfolio.

The fund is managed according to the guidelines provided by the mandate, diligently maintaining

adequate liquidity levels while keeping return volatility low. Term risk is carefully monitored, ensuring

that the weighted average duration remains within limits and is adjusted as the interest rate

environment changes.

Comment on the year ahead and, if possible, estimate the performance of your fund over 2 or

3 years. What are your targets and objectives for the year ahead?

Growth, as measured by GDP, is expected to remain below long-run historical averages due

to persistent structural challenges in the country. Earlier in the year, we were more optimistic that

improved reliability from Eskom’s electricity supply, combined with accelerated private investment

in renewable energy and stronger maintenance efforts, would improve business conditions and

support growth. However, we have since revised our growth expectations lower for 2025 and the

outer years, as global tariff pressures have created a highly unpredictable environment and domestic

economic activity has been weaker than anticipated.

While it is not the nature of a money market fund to predict returns, we take pride in our consistent

ability to deliver inflation-beating performance within mandate parameters. This remains exactly

what is required from this asset class.

Give your views regarding interest rate trends and the yield curve over the next 1 to 2 years.

What interest rates can investors expect? Do you anticipate further repo rate cuts?

At the July 2025 Monetary Policy Meeting, the governor announced that the SARB will now aim

to anchor inflation expectations at the lower end of the official 3% to 6% target range set by the

National Treasury, at 3%, rather than the previous midpoint of 4.5%. This decision followed extensive

consultation and research, which highlighted that South Africa is an outlier among emerging market

peers due to one of the widest inflation target ranges. The analysis also showed that this has

contributed to relatively higher general price levels compared to other emerging markets.

Although inflation may edge higher as fuel price base effects fade and food inflation rises, we

believe it remains well contained for the foreseeable future, supported by relatively stable oil prices,

a stable rand, and lower inflation expectations following the revised target.

Looking ahead over the next two years, we expect continued central bank action domestically.

The SARB’s Quarterly Projection Model (QPM), which forecasts key variables such as inflation

and output growth by combining historical data with structural economic relationships, projects

lower inflation under this 3% anchoring scenario. This should provide room for further monetary

accommodation through gradual rate cuts over the next two years.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

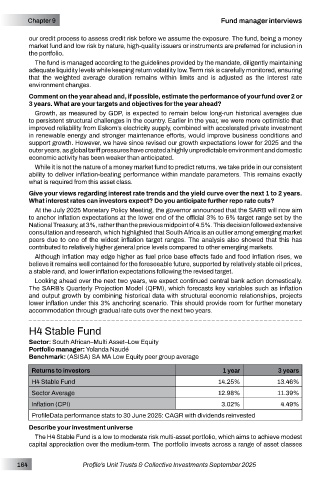

H4 Stable Fund

Sector: South African–Multi Asset–Low Equity

Portfolio manager: Yolanda Naudé

Benchmark: (ASISA) SA MA Low Equity peer group average

Returns to investors 1 year 3 years

H4 Stable Fund 14.25% 13.46%

Sector Average 12.98% 11.39%

Inflation (CPI) 3.02% 4.49%

ProfileData performance stats to 30 June 2025: CAGR with dividends reinvested

Describe your investment universe

The H4 Stable Fund is a low to moderate risk multi-asset portfolio, which aims to achieve modest

capital appreciation over the medium-term. The portfolio invests across a range of asset classes

164 Profile’s Unit Trusts & Collective Investments September 2025