Page 61 - Profile's Unit Trusts & Collective Investments - March 2026

P. 61

Costs and pricing Chapter 3

Because RiY is a forward-looking estimate, it has several limitations:

R It depends on projected returns, which are unknown. Lower projected returns make RiY appear

smaller, even though costs haven’t changed.

R It includes upfront costs, so the RiY improves over longer time periods as once-off charges are

spread out.

R It ignores penalties for reducing or stopping contributions, which can materially affect

outcomes.

R It can be manipulated by choosing optimistic growth assumptions or long projection periods.

For these reasons, RiY is a rough indicator rather than a precise measure of total costs. It can be

useful for comparisons, but it should be interpreted with caution.

Retirement savings cost (RSC) disclosure

The RSC, effective from March 2019, is designed to assist potential and existing employers

and/or boards of trustees (referred to as “clients” in the ASISA standard) when comparing retirement

fund quotations.

The RSC differs from the EAC because the latter is aimed at individuals. The RSC is aimed at

employers and trustees, it is not a member level cost disclosure standard and is not designed for

individual fund members.

For products that combine life cover and investment plans, the RSC applies to the savings

element only.

The RSC Disclosure Standard does not apply to RA funds (including group RA funds),

preservation funds, beneficiary funds, compulsory annuities and other retail products provided that

they are disclosing the EAC.

The template must show four separate components into which defined charges are allocated over

four investment periods:

R Investment management charges

R Advice charges

R Administration charges

R Other charges including regulatory, compliance and governance costs

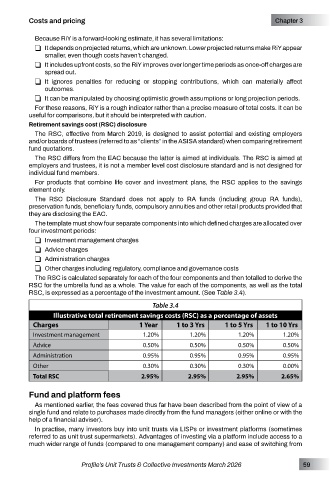

The RSC is calculated separately for each of the four components and then totalled to derive the

RSC for the umbrella fund as a whole. The value for each of the components, as well as the total

RSC, is expressed as a percentage of the investment amount. (See Table 3.4).

Table 3.4

Illustrative total retirement savings costs (RSC) as a percentage of assets

Charges 1 Year 1 to 3 Yrs 1 to 5 Yrs 1 to 10 Yrs

Investment management 1.20% 1.20% 1.20% 1.20%

Advice 0.50% 0.50% 0.50% 0.50%

Administration 0.95% 0.95% 0.95% 0.95%

Other 0.30% 0.30% 0.30% 0.00%

Total RSC 2.95% 2.95% 2.95% 2.65%

Fund and platform fees

As mentioned earlier, the fees covered thus far have been described from the point of view of a

single fund and relate to purchases made directly from the fund managers (either online or with the

help of a financial adviser).

In practise, many investors buy into unit trusts via LISPs or investment platforms (sometimes

referred to as unit trust supermarkets). Advantages of investing via a platform include access to a

much wider range of funds (compared to one management company) and ease of switching from

Profile’s Unit Trusts & Collective Investments March 2026 59