Page 60 - Profile's Unit Trusts & Collective Investments - March 2026

P. 60

Chapter 3 Costs and pricing

The EAC comprises four components which are calculated separately and then combined to

reflect the total EAC:

R Investment management charges (IMC): costs and charges associated with management of

all underlying investment portfolios

R Advice charges: initial and annual fees, both lump sum and recurring

R Administration charges: all costs of administration

R Other charges: a category for all remaining costs, including exit charges, penalties, loyalty

bonuses, guarantees, smoothing or risk benefits, wrap fund charges and risk benefits (such

as waiver of premium)

Four mandatory disclosure periods are required, as illustrated in Table 3.3. For open-ended

products this is one, three, five and 10 years. For “term” products the 10-year column must reflect

the “end of term” period, as defined, or age 55 term in the case of an RA or other retirement product.

The need for disclosure periods arises because of once-off costs. In the case of unit trusts, for

example, a compulsory initial charge that is expressed as a percentage of a lump sum investment

must be amortised on a straight line basis over the relevant disclosure period (ie, the initial charge is

divided by the number of years).

The EAC must be calculated once a year by end March (using data up to 31 December).

Technically, the EAC standard provides for a combination of calculation methodologies in order

to cope with the wide range of products to which it applies. Like reduction in yield (RiY), EAC is

a forward projection, but certain costs must be based on historical data (eg, for IMC, the TER

principles are specified). Where an RiY methodology has to be used (for example, where a payout

depends on the term and the capital value on termination), the EAC standard specifies a growth rate

of 6% per annum (gross).

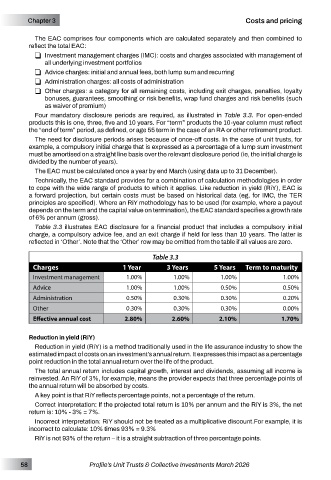

Table 3.3 illustrates EAC disclosure for a financial product that includes a compulsory initial

charge, a compulsory advice fee, and an exit charge if held for less than 10 years. The latter is

reflected in ‘Other’. Note that the ‘Other’ row may be omitted from the table if all values are zero.

Table 3.3

Charges 1 Year 3 Years 5 Years Term to maturity

Investment management 1.00% 1.00% 1.00% 1.00%

Advice 1.00% 1.00% 0.50% 0.50%

Administration 0.50% 0.30% 0.30% 0.20%

Other 0.30% 0.30% 0.30% 0.00%

Effective annual cost 2.80% 2.60% 2.10% 1.70%

Reduction in yield (RiY)

Reduction in yield (RiY) is a method traditionally used in the life assurance industry to show the

estimated impact of costs on an investment’s annual return. It expresses this impact as a percentage

point reduction in the total annual return over the life of the product.

The total annual return includes capital growth, interest and dividends, assuming all income is

reinvested. An RiY of 3%, for example, means the provider expects that three percentage points of

the annual return will be absorbed by costs.

A key point is that RiY reflects percentage points, not a percentage of the return.

Correct interpretation: If the projected total return is 10% per annum and the RiY is 3%, the net

return is: 10% - 3% = 7%.

Incorrect interpretation: RiY should not be treated as a multiplicative discount.For example, it is

incorrect to calculate: 10% times 93% = 9.3%

RiY is not 93% of the return – it is a straight subtraction of three percentage points.

58 Profile’s Unit Trusts & Collective Investments March 2026