Page 54 - Profile's Unit Trusts & Collective Investments - March 2026

P. 54

Chapter 3 Costs and pricing

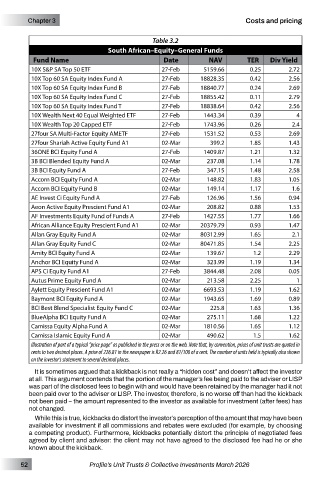

Table 3.2

South African–Equity–General Funds

Fund Name Date NAV TER Div Yield

10X S&P SA Top 50 ETF 27-Feb 5159.66 0.25 2.72

10X Top 60 SA Equity Index Fund A 27-Feb 18828.35 0.42 2.56

10X Top 60 SA Equity Index Fund B 27-Feb 18840.77 0.24 2.69

10X Top 60 SA Equity Index Fund C 27-Feb 18855.42 0.11 2.79

10X Top 60 SA Equity Index Fund T 27-Feb 18838.64 0.42 2.56

10X Wealth Next 40 Equal Weighted ETF 27-Feb 1443.34 0.39 4

10X Wealth Top 20 Capped ETF 27-Feb 1743.96 0.26 2.4

27four SA Multi-Factor Equity AMETF 27-Feb 1531.52 0.53 2.69

27four Shariah Active Equity Fund A1 02-Mar 399.2 1.85 1.43

36ONE BCI Equity Fund A 27-Feb 1409.87 1.21 1.32

3B BCI Blended Equity Fund A 02-Mar 237.08 1.14 1.78

3B BCI Equity Fund A 27-Feb 347.15 1.48 2.58

Accorn BCI Equity Fund A 02-Mar 148.82 1.83 1.05

Accorn BCI Equity Fund B 02-Mar 149.14 1.17 1.6

AE Invest Ci Equity Fund A 27-Feb 126.96 1.56 0.94

Aeon Active Equity Prescient Fund A1 02-Mar 208.82 0.88 1.53

AF Investments Equity Fund of Funds A 27-Feb 1427.55 1.77 1.66

African Alliance Equity Prescient Fund A1 02-Mar 20379.79 0.93 1.47

Allan Gray Equity Fund A 02-Mar 80312.99 1.65 2.1

Allan Gray Equity Fund C 02-Mar 80471.85 1.54 2.25

Amity BCI Equity Fund A 02-Mar 139.67 1.2 2.29

Anchor BCI Equity Fund A 02-Mar 323.99 1.19 1.34

APS Ci Equity Fund A1 27-Feb 3844.48 2.08 0.05

Autus Prime Equity Fund A 02-Mar 213.58 2.25 1

Aylett Equity Prescient Fund A1 02-Mar 6693.53 1.19 1.62

Baymont BCI Equity Fund A 02-Mar 1943.65 1.69 0.89

BCI Best Blend Specialist Equity Fund C 02-Mar 225.8 1.63 1.36

BlueAlpha BCI Equity Fund A 02-Mar 275.11 1.68 1.22

Camissa Equity Alpha Fund A 02-Mar 1810.56 1.65 1.12

Camissa Islamic Equity Fund A 02-Mar 490.62 1.5 1.62

Illustration of part of a typical “price page” as published in the press or on the web. Note that, by convention, prices of unit trusts are quoted in

cents to two decimal places. A price of 226.81 in the newspaper is R2.26 and 81/100 of a cent. The number of units held is typically also shown

on the investor’s statement to several decimal places.

It is sometimes argued that a kickback is not really a “hidden cost” and doesn’t affect the investor

at all. This argument contends that the portion of the manager’s fee being paid to the adviser or LISP

was part of the disclosed fees to begin with and would have been retained by the manager had it not

been paid over to the adviser or LISP. The investor, therefore, is no worse off than had the kickback

not been paid – the amount represented to the investor as available for investment (after fees) has

not changed.

While this is true, kickbacks do distort the investor’s perception of the amount that may have been

available for investment if all commissions and rebates were excluded (for example, by choosing

a competing product). Furthermore, kickbacks potentially distort the principle of negotiated fees

agreed by client and adviser: the client may not have agreed to the disclosed fee had he or she

known about the kickback.

52 Profile’s Unit Trusts & Collective Investments March 2026