Page 51 - Profile's Unit Trusts & Collective Investments - March 2026

P. 51

Costs and pricing Chapter 3

Annual costs are not the only issue. Entry costs such as

initial charges or upfront advice fees also have an impact. Real returns

Today, very few managers or platforms charge product- Real returns can be defined as net

level initial fees, and most advice fees must be explicitly investment returns achieved after

agreed to and authorised by the client under current inflation. If inflation was 4% over the

disclosure regulations. However, upfront advice fees year and a portfolio achieved 6% growth, the real

are still used in certain distribution models, particularly return was 2%. Rates of return before inflation are

by tied agents and on some investment products sold to called nominal returns.

lower-income earners.

When an initial advice fee is charged, the impact can be significant. At an upfront fee of 3.45%,

investors pay R3 450 for every R100 000 invested. In a fund achieving 10% per annum, this

difference compounds to more than R23 000 over 20 years. It might be argued that this is not a

significant difference given that R96 550 (the capital invested after payment of the upfront fee)

would still grow to almost R650 000 over the same period, and that 3.45% is a reasonable price to

pay for sound financial advice. However, R23 000 is not an insignificant amount. It highlights the

importance of evaluating fees against the quality of advice received. There is little benefit in saving

on costs but ending up in an inappropriate or mediocre fund. On the other hand, there is equally little

value in paying advice fees only to be placed in an expensive active fund that underperforms lower-

cost passive alternatives.

Transactions

Conceptually, the calculation of a price on a daily basis for each participatory interest in a CIS is

straightforward: the market value of the portfolio is calculated, and this is divided by the number of

units in issue.

From the point of view of the management company, things are slightly more complicated. For a

start, market values may need to be obtained from a number of different markets, both in SA and

overseas. Once an accurate portfolio valuation is in place, the pricing department also deals with:

R Accrual of all interest and dividends due to the portfolio

R Distribution of interest and dividends when applicable

R Any liabilities against the fund (such as service fees, accrued audit fees, trustee fees, and so on)

In a large management company, the administration department will provide the pricing

department with the number of units in issue at the close of trade, taking into account the sales of

units, repurchases of units, and any switches that have taken place.

The final price of each participatory interest, known as the net asset value price, can now be

calculated by dividing the net portfolio value by the number of units. This is the price published in the

daily and weekly newspapers, and is also the price at which units are repurchased.

Purchase and repurchase

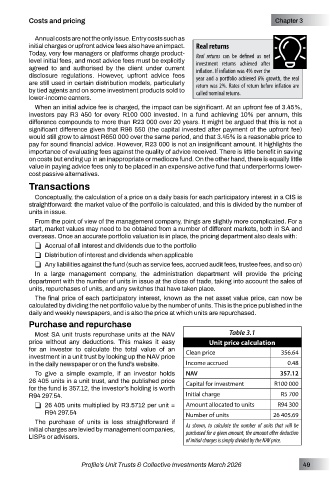

Most SA unit trusts repurchase units at the NAV Table 3.1

price without any deductions. This makes it easy Unit price calculation

for an investor to calculate the total value of an Clean price 356.64

investment in a unit trust by looking up the NAV price

in the daily newspaper or on the fund’s website. Income accrued 0.48

To give a simple example, if an investor holds NAV 357.12

26 405 units in a unit trust, and the published price Capital for investment R100 000

for the fund is 357.12, the investor’s holding is worth

R94 297.54. Initial charge R5 700

R 26 405 units multiplied by R3.5712 per unit = Amount allocated to units R94 300

R94 297.54 Number of units 26 405.69

The purchase of units is less straightforward if

initial charges are levied by management companies, As shown, to calculate the number of units that will be

LISPs or advisers. purchased for a given amount, the amount after deduction

of initial charges is simply divided by the NAV price.

Profile’s Unit Trusts & Collective Investments March 2026 49