Page 115 - Profile's Unit Trusts & Collective Investments - March 2026

P. 115

Investment risk Chapter 6

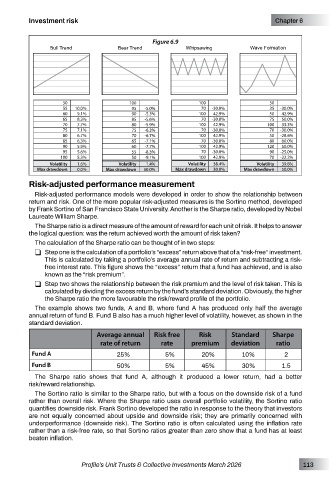

Figure 6.9

Bull Trend Bear Trend Whipsawing Wave Formation

50 100 100 50

55 10.0% 95 -5.0% 70 -30.0% 35 -30.0%

60 9.1% 90 -5.3% 100 42.9% 50 42.9%

65 8.3% 85 -5.6% 70 -30.0% 75 50.0%

70 7.7% 80 -5.9% 100 42.9% 100 33.3%

75 7.1% 75 -6.3% 70 -30.0% 70 -30.0%

80 6.7% 70 -6.7% 100 42.9% 50 -28.6%

85 6.3% 65 -7.1% 70 -30.0% 80 60.0%

90 5.9% 60 -7.7% 100 42.9% 120 50.0%

95 5.6% 55 -8.3% 70 -30.0% 90 -25.0%

100 5.3% 50 -9.1% 100 42.9% 70 -22.2%

Volatility 1.6% Volatility 1.4% Volatility 38.4% Volatility 39.8%

Max drawdown 0.0% Max drawdown 50.0% Max drawdown 30.0% Max drawdown 50.0%

Risk-adjusted performance measurement

Risk-adjusted performance models were developed in order to show the relationship between

return and risk. One of the more popular risk-adjusted measures is the Sortino method, developed

by Frank Sortino of San Francisco State University. Another is the Sharpe ratio, developed by Nobel

Laureate William Sharpe.

The Sharpe ratio is a direct measure of the amount of reward for each unit of risk. It helps to answer

the logical question: was the return achieved worth the amount of risk taken?

The calculation of the Sharpe ratio can be thought of in two steps:

R Step one is the calculation of a portfolio’s “excess” return above that of a “risk-free” investment.

This is calculated by taking a portfolio’s average annual rate of return and subtracting a risk-

free interest rate. This figure shows the “excess” return that a fund has achieved, and is also

known as the “risk premium”.

R Step two shows the relationship between the risk premium and the level of risk taken. This is

calculated by dividing the excess return by the fund’s standard deviation. Obviously, the higher

the Sharpe ratio the more favourable the risk/reward profile of the portfolio.

The example shows two funds, A and B, where fund A has produced only half the average

annual return of fund B. Fund B also has a much higher level of volatility, however, as shown in the

standard deviation.

Average annual Risk free Risk Standard Sharpe

rate of return rate premium deviation ratio

Fund A 25% 5% 20% 10% 2

Fund B 50% 5% 45% 30% 1.5

The Sharpe ratio shows that fund A, although it produced a lower return, had a better

risk/reward relationship.

The Sortino ratio is similar to the Sharpe ratio, but with a focus on the downside risk of a fund

rather than overall risk. Where the Sharpe ratio uses overall portfolio volatility, the Sortino ratio

quantifies downside risk. Frank Sortino developed the ratio in response to the theory that investors

are not equally concerned about upside and downside risk; they are primarily concerned with

underperformance (downside risk). The Sortino ratio is often calculated using the inflation rate

rather than a risk-free rate, so that Sortino ratios greater than zero show that a fund has at least

beaten inflation.

Profile’s Unit Trusts & Collective Investments March 2026 113