Page 159 - Profile's Unit Trusts & Collective Investments - March 2026

P. 159

Fund manager interviews Chapter 9

We believe SARB has established a strong and credible track record in containing inflation and

has earned the right for South African administered rates to continue compressing towards levels

observed in more developed markets. Accordingly, we expect to see additional compression in the

10-year yield and have revised our short rate expectations lower and now anticipate a further 50bps

to 75bps of rate cuts in 2026, taking the terminal repo rate to approximately 6.00% to 6.25%.

Further details on the fund can be found in the latest fund factsheet.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

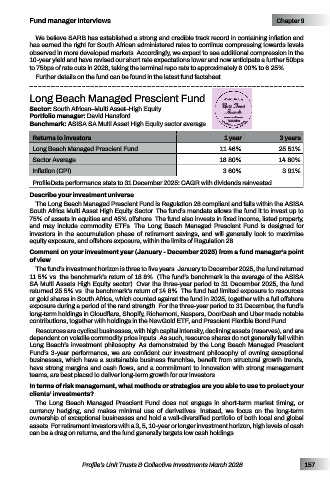

Long Beach Managed Prescient Fund

Sector: South African–Multi Asset–High Equity Unit Trust

Awards

Portfolio manager: David Hansford 2026

WINNER

Benchmark: ASISA SA Multi Asset High Equity sector average For performance to 31 December 2025

Returns to investors 1 year 3 years

Long Beach Managed Prescient Fund 11.46% 25.51%

Sector Average 18.80% 14.80%

Inflation (CPI) 3.60% 3.91%

ProfileData performance stats to 31 December 2025: CAGR with dividends reinvested

Describe your investment universe

The Long Beach Managed Prescient Fund is Regulation 28 compliant and falls within the ASISA

South Africa Multi Asset High Equity Sector. The fund’s mandate allows the fund it to invest up to

75% of assets in equities and 45% offshore. The fund also invests in fixed income, listed property,

and may include commodity ETFs. The Long Beach Managed Prescient Fund is designed for

investors in the accumulation phase of retirement savings, and will generally look to maximise

equity exposure, and offshore exposure, within the limits of Regulation 28.

Comment on your investment year (January - December 2025) from a fund manager’s point

of view

The fund’s investment horizon is three to five years. January to December 2025, the fund returned

11.5% vs. the benchmark’s return of 18.8%. (The fund’s benchmark is the average of the ASISA

SA Multi Assets High Equity sector). Over the three-year period to 31 December 2025, the fund

returned 25.5% vs. the benchmark’s return of 14.8%. The fund had limited exposure to resources

or gold shares in South Africa, which counted against the fund in 2025, together with a full offshore

exposure during a period of the rand strength. For the three-year period to 31 December, the fund’s

long-term holdings in Cloudflare, Shopify, Richemont, Naspers, DoorDash and Uber made notable

contributions, together with holdings in the NewGold ETF, and Prescient Flexible Bond Fund.

Resources are cyclical businesses, with high capital intensity, declining assets (reserves), and are

dependent on volatile commodity price inputs. As such, resource shares do not generally fall within

Long Beach’s investment philosophy. As demonstrated by the Long Beach Managed Prescient

Fund’s 3-year performance, we are confident our investment philosophy of owning exceptional

businesses, which have a sustainable business franchise, benefit from structural growth trends,

have strong margins and cash flows, and a commitment to innovation with strong management

teams, are best placed to deliver long-term growth for our investors.

In terms of risk management, what methods or strategies are you able to use to protect your

clients’ investments?

The Long Beach Managed Prescient Fund does not engage in short-term market timing, or

currency hedging, and makes minimal use of derivatives. Instead, we focus on the long-term

ownership of exceptional businesses and hold a well-diversified portfolio of both local and global

assets. For retirement investors with a 3, 5, 10-year or longer investment horizon, high levels of cash

can be a drag on returns, and the fund generally targets low cash holdings.

Profile’s Unit Trusts & Collective Investments March 2026 157