Page 157 - Profile's Unit Trusts & Collective Investments - March 2026

P. 157

Fund manager interviews Chapter 9

not experienced for some time. Nevertheless, while we therefore expect a cyclical upturn, structural

growth remains subdued but should also gradually lift as structural reforms assert themselves.

We believe we will continue to achieve our CPI + 3% target while also achieving:

A high degree of capital preservation over rolling 12 months

Consistent inflation beating returns over rolling 36 months.

Are equity markets in general overpriced? Do you anticipate a significant correction?

We are still constructive on domestic equity.

The global risk-on rally extended into 2026 with equities rising in the first 2 months of the year. We

have seen increased volatility around gold and platinum stocks with investors trying to determine if

the rally over the last year has been too much. We have seen some signs of broad-based strength,

led by precious metals and banks. Despite the strong run in equities our 12-month expected return

holds at 10%, underpinned by continued earnings upgrades in precious-metal stocks.

Overall, we remain constructive on domestic equities, supported by the ongoing economic

recovery and strong EM fundamentals especially amid falling developed market interest rates and

a weaker dollar. While key domestic risks such as GNU uncertainty, U.S.-SA relations, and tariff

threats have moderated, stretched valuations in developed markets remain a concern.

Global equity valuation multiples remain elevated, trading approximately one standard deviation

above historical averages as the market rally extends. This is particularly evident in the US, where

valuations are stretched. While anticipated AI-driven productivity gains and a shift toward looser

monetary and fiscal policy are supporting earnings upgrades into 2026 – especially in the US

– emerging markets are also poised to benefit from lower developed market interest rates and a

weaker dollar. Despite this constructive fundamental backdrop, these favourable expectations

appear to be largely reflected in current elevated valuations.

Which asset classes do you expect will give the best total rates of return over the next few

years?

We believe in building a diversified portfolio from assets that have the highest probability of

achieving our return objective of inflation + 3%. At present we still prefer local assets to foreign.

We continue to look at opportunities in the market with an ongoing assessment of future expected

returns as explained above in our active asset allocation process.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

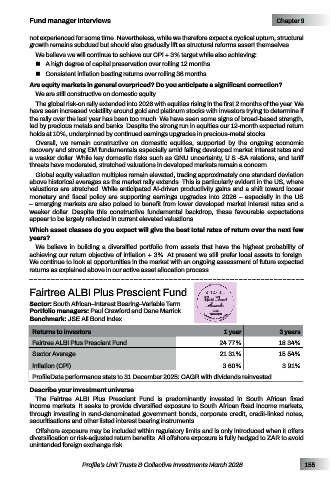

Fairtree ALBI Plus Prescient Fund

Sector: South African–Interest Bearing–Variable Term Unit Trust

Awards

Portfolio managers: Paul Crawford and Dane Marrick For performance to 31 December 2025

2026

Benchmark: JSE All Bond Index WINNER

Returns to investors 1 year 3 years

Fairtree ALBI Plus Prescient Fund 24.77% 18.34%

Sector Average 21.31% 15.54%

Inflation (CPI) 3.60% 3.91%

ProfileData performance stats to 31 December 2025: CAGR with dividends reinvested

Describe your investment universe

The Fairtree ALBI Plus Prescient Fund is predominantly invested in South African fixed

income markets. It seeks to provide diversified exposure to South African fixed income markets,

through investing in rand-denominated government bonds, corporate credit, credit-linked notes,

securitisations and other listed interest bearing instruments.

Offshore exposure may be included within regulatory limits and is only introduced when it offers

diversification or risk-adjusted return benefits. All offshore exposure is fully hedged to ZAR to avoid

unintended foreign exchange risk.

Profile’s Unit Trusts & Collective Investments March 2026 155