Page 147 - Profile's Unit Trusts & Collective Investments - March 2026

P. 147

Classification of CISs Chapter 8

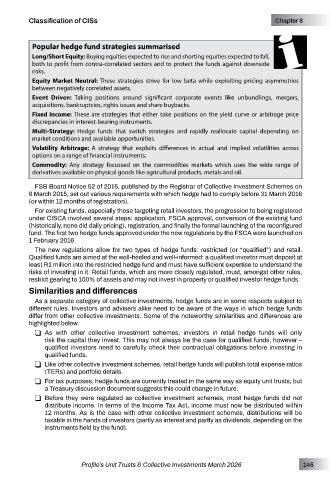

Popular hedge fund strategies summarised

Long/Short Equity: Buying equities expected to rise and shorting equities expected to fall,

both to profit from contra-correlated sectors and to protect the funds against downside

risks.

Equity Market Neutral: These strategies strive for low beta while exploiting pricing asymmetries

between negatively correlated assets.

Event Driven: Taking positions around significant corporate events like unbundlings, mergers,

acquisitions, bankruptcies, rights issues and share buybacks.

Fixed Income: These are strategies that either take positions on the yield curve or arbitrage price

discrepancies in interest-bearing instruments.

Multi-Strategy: Hedge funds that switch strategies and rapidly reallocate capital depending on

market conditions and available opportunities.

Volatility Arbitrage: A strategy that exploits differences in actual and implied volatilities across

options on a range of financial instruments.

Commodity: Any strategy focussed on the commodities markets which uses the wide range of

derivatives available on physical goods like agricultural products, metals and oil.

FSB Board Notice 52 of 2015, published by the Registrar of Collective Investment Schemes on

6 March 2015, set out various requirements with which hedge had to comply before 31 March 2016

(or within 12 months of registration).

For existing funds, especially those targeting retail investors, the progression to being registered

under CISCA involved several steps: application, FSCA approval, conversion of the existing fund

(historically, none did daily pricing), registration, and finally the formal launching of the reconfigured

fund. The first two hedge funds approved under the new regulations by the FSCA were launched on

1 February 2016.

The new regulations allow for two types of hedge funds: restricted (or “qualified”) and retail.

Qualified funds are aimed at the well-heeled and well-informed: a qualified investor must deposit at

least R1 million into the restricted hedge fund and must have sufficient expertise to understand the

risks of investing in it. Retail funds, which are more closely regulated, must, amongst other rules,

restrict gearing to 100% of assets and may not invest in property or qualified investor hedge funds.

Similarities and differences

As a separate category of collective investments, hedge funds are in some respects subject to

different rules. Investors and advisers alike need to be aware of the ways in which hedge funds

differ from other collective investments. Some of the noteworthy similarities and differences are

highlighted below.

R As with other collective investment schemes, investors in retail hedge funds will only

risk the capital they invest. This may not always be the case for qualified funds, however –

qualified investors need to carefully check their contractual obligations before investing in

qualified funds.

R Like other collective investment schemes, retail hedge funds will publish total expense ratios

(TERs) and portfolio details.

R For tax purposes, hedge funds are currently treated in the same way as equity unit trusts, but

a Treasury discussion document suggests this could change in future.

R Before they were regulated as collective investment schemes, most hedge funds did not

distribute income. In terms of the Income Tax Act, income must now be distributed within

12 months. As is the case with other collective investment schemes, distributions will be

taxable in the hands of investors (partly as interest and partly as dividends, depending on the

instruments held by the fund).

Profile’s Unit Trusts & Collective Investments March 2026 145