Page 90 - Profile's Unit Trusts & Collective Investments - March 2026

P. 90

Chapter 5 Legislation and guidelines

The RDR proposed several regulatory reforms related to the provision of financial advice and

the distribution of financial products. Amongst other things, the RDR sought to incorporate the

principles contained in the FSCA’s TCF code.

A number of the RDR proposals have been implemented while others will be implemented using

a combination of instruments available under existing financial sector laws (such as the Financial

Sector Regulation Act) and the planned Conduct of Financial Institutions (COFI) Act.

One of the RDR prosposals was to introduce new terminology, including product supplier agent

(PSA) for tied broker and registered financial adviser (RFA), for an independent financial adviser

(IFA). The proposed RDR suggested PSAs would need to state that they do not offer independent

advice but merely represent the products of their employer.

These proposals have been put on hold pending the enactment of the COFI Bill when the

terminology used for financial advisers will be aligned to the licences that are issued for diffrent

activities.

The RDR proposals included attempts to more clearly delineate intermediation activities,

outsourced services and advice. The FSCA was considering several possible legislative proposals,

including:

R rules to facilitate the charging of advice fees separate from commissions in order to achieve a

clear demarcation of advice and “services as intermediary”;

R an approval process to replace the current outsourcing notification process, plus further

reporting requirements in respect of outsourcing.

Another RDR proposal that may be considered after COFI is enacted sought to stop agents

earning recurring fees unless the financial adviser is providing recurring advice. Currently many

financial advisers earn commission on recurring monthly payments (such as debit orders) even if

they do not see clients regularly to review their portfolios, needs and risk profiles.

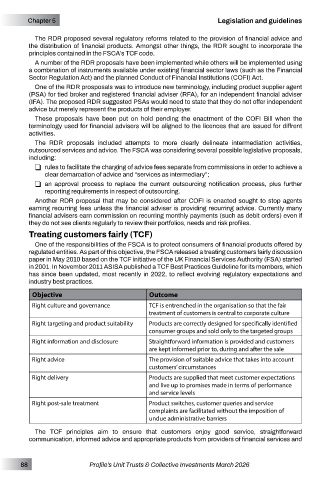

Treating customers fairly (TCF)

One of the responsibilities of the FSCA is to protect consumers of financial products offered by

regulated entities. As part of this objective, the FSCA released a treating customers fairly discussion

paper in May 2010 based on the TCF initiative of the UK Financial Services Authority (FSA) started

in 2001. In November 2011 ASISA published a TCF Best Practices Guideline for its members, which

has since been updated, most recently in 2022, to reflect evolving regulatory expectations and

industry best practices.

Objective Outcome

Right culture and governance TCF is entrenched in the organisation so that the fair

treatment of customers is central to corporate culture

Right targeting and product suitability Products are correctly designed for specifically identified

consumer groups and sold only to the targeted groups

Right information and disclosure Straightforward information is provided and customers

are kept informed prior to, during and after the sale

Right advice The provision of suitable advice that takes into account

customers’ circumstances

Right delivery Products are supplied that meet customer expectations

and live up to promises made in terms of performance

and service levels

Right post-sale treatment Product switches, customer queries and service

complaints are facilitated without the imposition of

undue administrative barriers

The TCF principles aim to ensure that customers enjoy good service, straightforward

communication, informed advice and appropriate products from providers of financial services and

88 Profile’s Unit Trusts & Collective Investments March 2026