Page 178 - Profile's Unit Trusts & Collective Investments - March 2026

P. 178

Chapter 9 Fund manager interviews

while many others (Nvidia) are generating a large portion of their earnings from this same data centre

spend. The economic returns of this AI spend are uncertain and it is a highly competitive space.

The primary companies and products in the AI space (OpenAI, Anthropic) are not yet profitable.

We can’t be certain that there will be a significant correction however, we don’t believe investors

are being adequately compensated for the risk they are taking at these valuations and earnings

levels. Companies in sectors less affected to AI disintermediation across the globe, certain well

capitalised South African companies and specific geographies such as Japan and India all provide

new avenues for measured portfolio diversification.

Which asset classes do you expect will give the best total rates of return over the next few

years?

Equities. Should government’s reforms materialise and the GDP growth rate improve, SA Inc

should do very well. Companies have survived a no growth environment for many years. They are

lean and highly leveraged to top line growth. Many of these companies trade at single digit multiples

and high dividend yield. Should the growth not materialise, we should still see double digit return

with low downside.

Activist positions, gold, energy and certain commodities. The US is continuing to compound

record levels of government debt while engaging in global military and economic warfare. The global

race for AI and energy investment will add further tailwinds to these asset classes.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

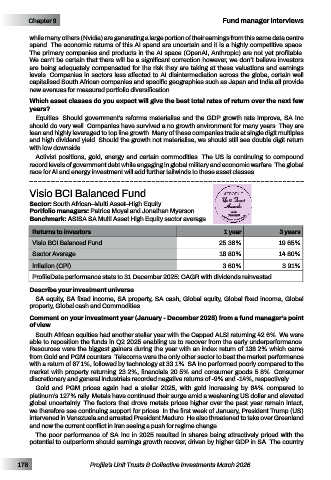

Visio BCI Balanced Fund

Sector: South African–Multi Asset–High Equity Unit Trust

Awards

Portfolio managers: Patrice Moyal and Jonathan Myerson 2026

Benchmark: ASISA SA Multi Asset High Equity sector average For performance to 31 December 2025

WINNER

Returns to investors 1 year 3 years

Visio BCI Balanced Fund 25.36% 19.65%

Sector Average 18.80% 14.80%

Inflation (CPI) 3.60% 3.91%

ProfileData performance stats to 31 December 2025: CAGR with dividends reinvested

Describe your investment universe

SA equity, SA fixed income, SA property, SA cash, Global equity, Global fixed income, Global

property, Global cash and Commodities.

Comment on your investment year (January - December 2025) from a fund manager’s point

of view

South African equities had another stellar year with the Capped ALSI returning 42.6%. We were

able to reposition the funds in Q2 2025 enabling us to recover from the early underperformance.

Resources were the biggest gainers during the year with an index return of 138.2% which came

from Gold and PGM counters. Telecoms were the only other sector to beat the market performance

with a return of 67.1%, followed by technology at 33.1%. SA Inc performed poorly compared to the

market with property returning 23.2%, financials 20.5% and consumer goods 5.8%. Consumer

discretionary and general industrials recorded negative returns of -9% and -14%, respectively.

Gold and PGM prices again had a stellar 2025, with gold increasing by 64% compared to

platinum’s 127% rally. Metals have continued their surge amid a weakening US dollar and elevated

global uncertainty. The factors that drove metals prices higher over the past year remain intact,

we therefore see continuing support for prices. In the first week of January, President Trump (US)

intervened in Venezuela and arrested President Maduro. He also threatened to take over Greenland

and now the current conflict in Iran seeing a push for regime change.

The poor performance of SA Inc in 2025 resulted in shares being attractively priced with the

potential to outperform should earnings growth recover, driven by higher GDP in SA. The country

176 Profile’s Unit Trusts & Collective Investments March 2026