Page 172 - Profile's Unit Trusts & Collective Investments - March 2026

P. 172

Chapter 9 Fund manager interviews

Furthermore, Taquanta manages a very large book of fixed income assets, which means we have

a sizeable internal market to generate or absorb liquidity when needed. This provides our clients with

a significant advantage in minimizing price and liquidity risk in their portfolios.

We apply strict spread discipline to ensure investments provide appropriate compensation for:

credit risk, liquidity risk, structural complexity and term risk.

Comment on the year ahead and, if possible, estimate the performance of your fund over 2 or

3 years. What are your targets and objectives for the year ahead?

Given the portfolio’s predominantly floating-rate exposure, nominal yields will adjust lower if rate

cuts filter through. While this reduces the base rate, we expect the portfolio to maintain a healthy

spread over JIBAR (and its successor reference rate). Considering the spread compression

witnessed and the fund’s maturity profile over the next two years, we conservatively estimate the

fund delivering in the region of JIBAR (or similar rate) +2.5% annually over the next 2 years.

Our objective remains to allocate selectively to assets that offer attractive yields on a risk-adjusted

basis, while preserving a low-volatility return profile.

Which asset classes do you expect will give the best total rates of return over the next few

years?

We look for best risk-adjusted rates of return. Within the investment universe we look at, we still

see selective value in certain forms of structured notes going forward. Whilst there could be further

yield compression, our focus remains on generating stable income rather than taking aggressive

interest rate bets.

Give your views regarding interest rate trends and the yield curve over the next 1 to 2 years.

What interest rates can investors expect? Do you anticipate further repo rate cuts?

Prior to the escalation in tensions involving the US, Iran and Israel, South African inflation

dynamics appeared broadly contained within SARB’s target band. However, the recent geopolitical

developments introduce renewed upside risks to the inflation outlook, mainly through potential

increases in global energy prices.

Before these events, the FRA curve had been pricing in roughly two 25 basis points interest rate

cuts over the next 12 months. In response to the increased geopolitical uncertainty, the forward

curve has flattened as markets reassess the outlook for inflation and monetary policy.

While this may delay the start of the easing cycle, our base case remains that the South-African

Reserve Bank will still have scope to lower interest rates over the longer term. The timing of these

cuts may, however, shift further out, potentially materialising later in 2026 or even into 2027 should

inflation risks persist.

For now, it remains unclear whether the current volatility represents a temporary disruption or

signals a more persistent shift in the global inflation environment.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

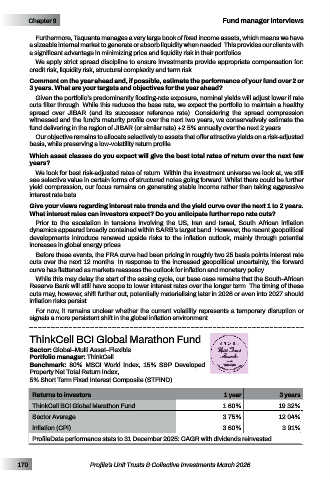

ThinkCell BCI Global Marathon Fund

Sector: Global–Multi Asset–Flexible Unit Trust

Portfolio manager: ThinkCell Awards

Benchmark: 80% MSCI World Index, 15% S&P Developed For performance to 31 December 2025

2026

WINNER

Property Net Total Return Index,

5% Short Term Fixed Interest Composite (STFIND)

Returns to investors 1 year 3 years

ThinkCell BCI Global Marathon Fund 1.60% 19.32%

Sector Average 3.75% 12.04%

Inflation (CPI) 3.60% 3.91%

ProfileData performance stats to 31 December 2025: CAGR with dividends reinvested

170 Profile’s Unit Trusts & Collective Investments March 2026